In the fourth quarter of 2025, there were 95 new initial public offerings (IPOs), which raised $23.6 billion. Total IPOs declined by 5% from the third quarter but total gross proceeds increased by 11% over Q3 2025.

Compared to Q4 2024, total IPOs increased by 20% from 79 to 95, while total IPO proceeds increased by 168% from $8.8 billion to $23.6 billion.

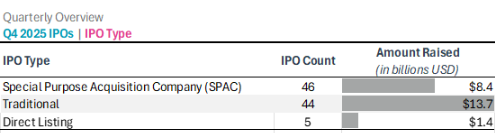

IPO type

There were 44 traditional IPOs this quarter, representing 46% of total public offerings for the quarter, as compared to 65% for Q3.

Special Purpose Acquisition Companies (SPACs) represented 48% of total IPOs in Q4 with a total of 46 new offerings. Compared to last quarter, SPAC IPOs increased by 31% while traditional IPOs decreased by 32%.

Traditional IPOs raised an average of $310.7 million per IPO, a 43% increase from the average of $217.5 million for traditional IPOs in Q3 2025. SPAC IPOs raised an average of $184.6 million per IPO in Q4 2025, 8% lower than average SPAC IPO proceeds from the previous quarter.

Unicorn IPO

During Q4 2025, there were two companies that raised over $1 billion in proceeds from their initial public offerings. Medline, a medical supply company, raised approximately $6.25 billion by selling 216 million shares at $29 per share. Medline used $4.0 billion of IPO proceeds to pay down their debt from their leveraged buy-out in 2021. BETA Technologies, Inc. is an aerospace company designing, manufacturing, and selling high-performance electric aircraft that sold 29 million shares at $34 per share.

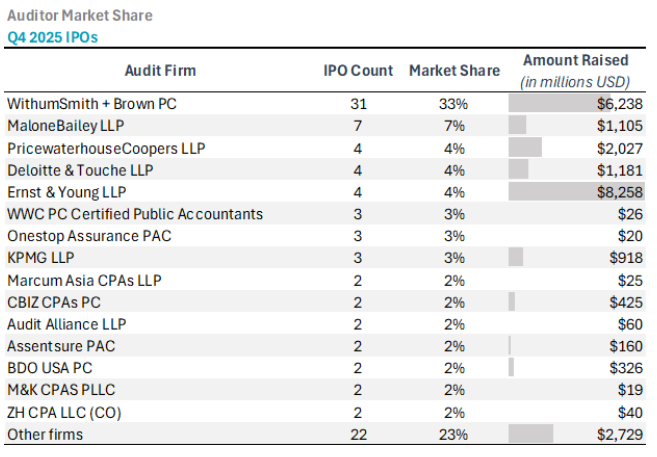

Auditor market share

Q4 2025 saw WithumSmith+Brown PC maintain its position as the leading IPO auditor by client count, auditing 31 IPOs for a 33% market share. MaloneBailey LLP came in second with 7 IPOs (7%), while PricewaterhouseCoopers, Deloitte, and EY each audited 4 IPOs (4% each). Despite EY's relatively modest client count, its clients raised a combined $8.3 billion, driven largely by the Medline Inc. IPO.

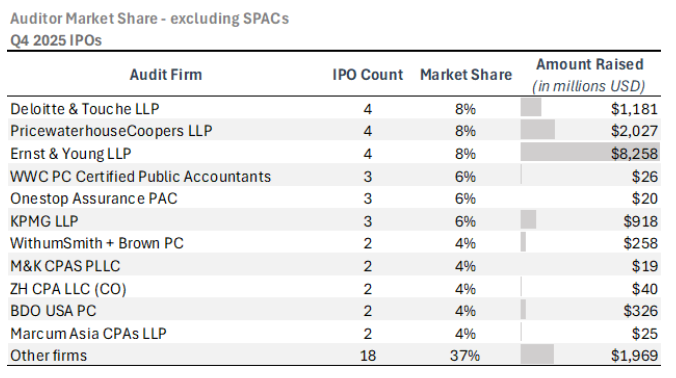

Excluding SPACs

Stripping out SPACs, the top three firms are from the Big Four. Deloitte, PricewaterhouseCoopers, and EY each audited 4 non-SPAC IPOs (8% market share each). KPMG rounded out the Big Four with 3 IPOs at 6% market share. WWC had three foreign private issuer IPOs, as did Onestop Assurance. WithumSmith+Brown dropped to 4% share (2 IPOs) in the non-SPAC segment, reflecting its concentration in the SPAC market.

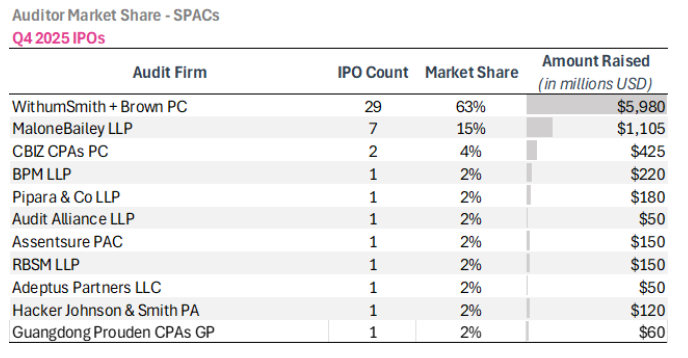

Auditor market share – SPACs

WithumSmith+Brown maintained its dominant position in the SPAC IPO market in Q4 2025, auditing 29 of the 46 SPAC IPOs and commanding a 63% market share. MaloneBailey LLP was a distant second with 7 SPAC IPOs (15%). CBIZ CPAs, which acquired former leader Marcum, audited 2 SPAC IPOs for a 4% share.

Read our report

Explore 2025 initial public offerings trends further in our latest IPO trends report. For a clear, data-driven look at two decades of market performance, fee benchmarks and the increasing role of global issuers.

Explore audit and regulatory disclosure data

Expert data you can trust – and find within seconds. Your go-to place for public accounting, governance and disclosure intelligence.